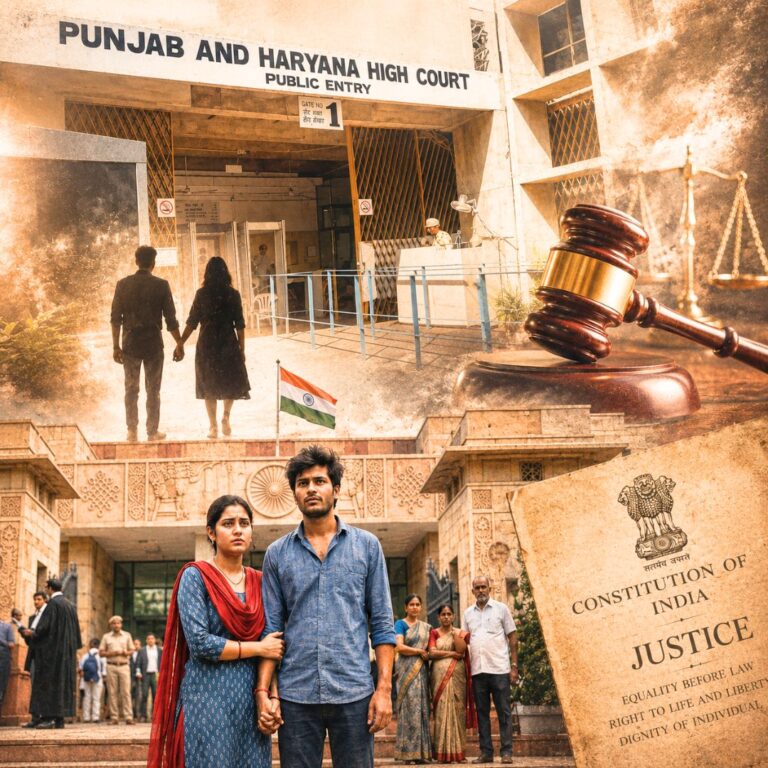

A story circulating widely on social media claims that a Bengaluru man lost his ₹1.2 crore flat after missing three home‑loan EMI payments following a job layoff, a sequence shared by his neighbour and chartered accountant Meenal Goel on LinkedIn that has reignited debate on financial planning and the risks of unsecured income reliance.

According to the post, the bank invoked the Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest (SARFAESI) Act, 2002, issued a default notice and auctioned the property within about 60 days for ₹95 lakh, leaving the borrower with just ₹15 lakh after eight years of payments.

While the narrative has been widely shared on X and reported by several news outlets, many readers, financial commentators and industry observers have raised doubts about the accuracy of key claims, including the timeline and sale price. No public statement has been made by the lending bank in this specific case, and major media emphasise that the original assertions are based on social media posts that have not been independently verified.

Viral Home Loss Sparks Skepticism

In a LinkedIn post first shared weeks ago, Bengaluru‑based CA Meenal Goel recounted that her neighbour identified only as “Rajesh” was laid off from his job in October 2025 and subsequently missed three consecutive EMI payments on his home loan by January 2026.

Goel wrote that the bank “sent him a notice under something called the SARFAESI Act and within 60 days, they auctioned his flat”, which he had originally purchased for ₹1.2 crore, but which reportedly fetched just ₹95 lakh at the auction. After eight years of payments, the account holder was said to have received only ₹15 lakh back while the bank retained around ₹80 lakh to settle outstanding dues.

“The bank recovered their ₹80 lakh outstanding. Rajesh got ₹15 lakhs back after eight years of payments,” Goel wrote, stressing that “one layoff destroyed eight years of work.” She went on to call the story a “cautionary tale” about the importance of financial planning, emergency savings and transparent dialogue with lenders when facing sudden income loss.

Observers on X echoed the cautionary tone, with user Amit Arora describing the episode as a stark reminder of how critical emergency funds and proactive financial management can be during periods of unemployment.

However, many readers and finance professionals have questioned details of the narrative. Critics have pointed out that an eight‑year‑old Bengaluru flat selling for below its purchase price is unusual given the city’s long‑term real‑estate appreciation, and that banks typically do not move as swiftly as described to auction properties after default.

Financial commentators note that a missed payment schedule and asset auction under SARFAESI involves multiple statutory stages before sale, making a 60‑day turnover from default to auction less plausible in a standard case.

Understanding SARFAESI and the Loan Default Process

The SARFAESI Act, 2002 empowers banks and financial institutions in India to recover dues of secured loans without needing to go through the civil courts, by taking possession of the secured assets and selling them to recover the outstanding amount. The Act is intended to strengthen asset recovery mechanisms and reduce the time and costs involved in loan recovery.

Under typical banking practice, if EMIs on a home loan are not paid, the account is first categorised under various stages of delinquency. According to loan‑recovery guidelines:

- A loan can be classified as a non‑performing asset (NPA) if payments remain overdue for more than 90 days.

- Before any action on the security can be taken under SARFAESI, banks must issue notices, allow the borrower a period to respond, and follow valuation and publication procedures for the asset before auction. Public notices inviting bids are generally required to be published at least 30 days before the actual auction date. Borrowers also have options to negotiate a one‑time settlement, seek loan restructuring, or approach the Debt Recovery Tribunal (DRT) to challenge the actions or seek relief.

These procedural requirements suggest that in many cases, especially where discussions, negotiations or legal processes are ongoing, the time between first missed EMI and auction can span several months. The assertion in the viral post that a property was auctioned within roughly two months has therefore been regarded as atypical rather than standard banking practice.

Broader Debate: Financial Literacy and Vulnerability

Independent of this specific claim’s accuracy, the story has struck a chord with many Indians grappling with long‑term financial commitments and the insecurity that can accompany sudden income loss. With rising costs of living, longer loan tenures stretching 15-30 years, and uncertain job markets particularly in sectors exposed to cyclical layoffs many middle‑class homebuyers are increasingly aware of how fragile perceived financial stability can be.

Financial advisors routinely emphasise the value of emergency savings, diversified income sources, and early engagement with lending institutions if payment difficulties arise. Lenders themselves, under Reserve Bank of India (RBI) protections, are expected to follow fair practices and offer avenues such as restructuring or moratoriums in genuine hardship cases before moving to enforcement.

The Logical Indian’s Perspective

Whether or not every detail of the viral narrative is entirely accurate, it has opened a vital conversation about the realities faced by individual borrowers outside abstract financial planning models. At its core, this story highlights vulnerabilities that many families experience when long‑term financial commitments collide with sudden life changes like job loss.

A Bengaluru resident lost his ₹1.20 crore flat after missing just three home loan EMIs due to job loss. The SARFAESI Act auctioned the flat for a mere ₹95 lakh.

— Amit Arora 🇮🇳 (@GuruShareMarket) March 2, 2026

CA Meenal Goel explained that her neighbour had been diligently paying EMIs for eight years. However, after default,…